FHA, VA, and USDA Loans — Your Questions, Answered.

With a surplus of mortgage loans, it can be hard to know which one is right for you. It can also be difficult to understand the different complexities of these loans, like who can get them and what the terms are. This article will focus specifically on FHA, VA, and USDA loans because these loans are more specific. Your questions answered on different loans will help clarify these options.

Federal Housing Administration (U.S.) Loan

These home loans are insured by the Federal Housing Administration. This means that they can offer a better deal, especially to first-time home buyers. However, they are available to anyone who meets the eligibility requirements. This loan type also accepts a variety of property types, including single-family homes.

You qualify for this loan if:

- You are a lawful U.S. citizen

- You have a credit score of 500 and above

- You have a minimum down payment of 3.5% to 10%

- Your home will be your primary residence

- Have steady employment

The benefits of this loan include:

- Lower down payment than conventional loans and down payment assistance

- Very low credit score requirements

- Lenient DTI (debt to income) ratio, but preferably below 43%

- Acceptance of financial gifts

- Multiple property types

Here are some other things to be aware of with this type of loan:

- You have to pay mortgage insurance each month, which can increase your monthly payments

- Your property must have an approved FHA appraisal to make sure it is up to good standards

An FHA loan is a great option for many people! If interested in getting this loan or learning more about it, talk to an expert and they can help you explore this option more.

Veterans Affairs Loan

A VA loan is a loan guaranteed by the U.S. Department of Veterans Affairs. These affordable home loans are created with flexible qualifications and great benefits!

The people who qualify for this loan include veterans, servicemembers, and eligible surviving spouses.

The benefits of this loan include:

- No down payment

- Low interest rates

- Limited closing costs

- No private mortgage insurance requirement

- Can use multiple times throughout life

- Foreclosure avoidance assistance

VA loans do come with a funding fee, but it varies based on factors such as military service and down payment. Though an added cost, it’s a one-time fee, and some borrowers may qualify for exemptions.

If interested in researching this loan option further, talk to an expert and learn more here.

United States Department of Agriculture Loan

This loan is supported by the government and makes home ownership affordable for those living in more rural areas. They focus on supporting rural economic development because by facilitating home purchases in less populated areas, these loans contribute to community growth.

To qualify for this loan, the rural area you want to live in must be approved. You also must have a certain household income, though assistance is often provided for low/very low income households. To get an estimate of eligible areas, check out this map.

Benefits of this loan include:

- No down payment

- Competitive fixed interest rates

- Not limited to who can apply

- Nontraditional credit sometimes accepted

Some other things to know with USDA loans include:

- The property needs to be a primary residence and meet certain safety standards and habitability guidelines.

- Borrowers pay an upfront guarantee fee, which can be rolled into the loan amount. An annual fee is also part of the loan structure (lower than a PMI though).

- The USDA also sets loan limits, which depend on the area. These limits ensure that the focus remains on affordable housing and that homes purchased meet reasonable cost criteria.

This can be a great option for those who might not have a high household income and want to live in a more rural area. Look into this option further or apply today!

Additional Tips

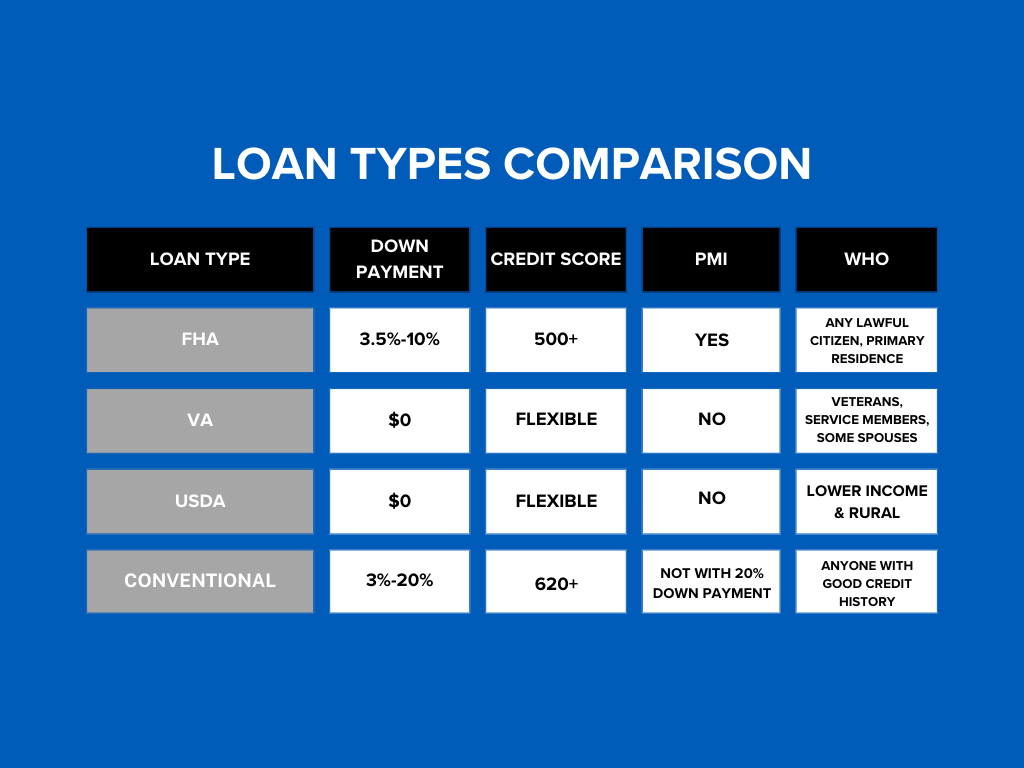

Here is a summary of how these loans and a conventional loan compare to each other:

Deciding which home loan to get can be a frustrating or difficult process. Looking at the requirements and benefits closely can help you in this journey and can bring you peace of mind when making a decision. Here are some other tips when choosing which home loan is best for you and your family:

- What are your long term plans for where you live?

- What are your short and long term financial goals?

- Where do you want to live and what lifestyle do you want to have?

Now you know some of the benefits and drawbacks of popular home loan options. By examining these factors, you can choose a loan that supports your homeownership dreams while fitting within your financial means.

- Previous

- Start Budgeting in 2025